Every technology that has been discovered or invented has its own advantages and downside too.

In some of the technologies the world has been witness to in the recent past the limitations could largely overshadow its utility. Even though blockchain technology has a reputation for being complex, its potential as a decentralized form of record keeping is limitless. Features such as privacy, higher security at lowered processing fees, and not being prone to errors are its USP.

And due to these advantages we may as well see applications of blockchain technology being imbibed more than other contemporary technologies present in the market right now.

Pros and Cons of blockchain technology

Pros

- Due to the segregation of the human involvement in verification there is enhanced accuracy

- Due to the elimination of third party verification cost is optimized

- The technology is tamper proof due to decentralization

- Transactions are private, protected and efficient

- Transparent technology

Cons

- Cost of technology is high due to mining bitcoin

- Speed of transactions per second is paltry

- Prevalent usage in illicit activities

- Vulnerability to hack is ever present

Also Read: Blockchain in Healthcare

Advantages of Blockchain Technology

Accuracy of the Chain

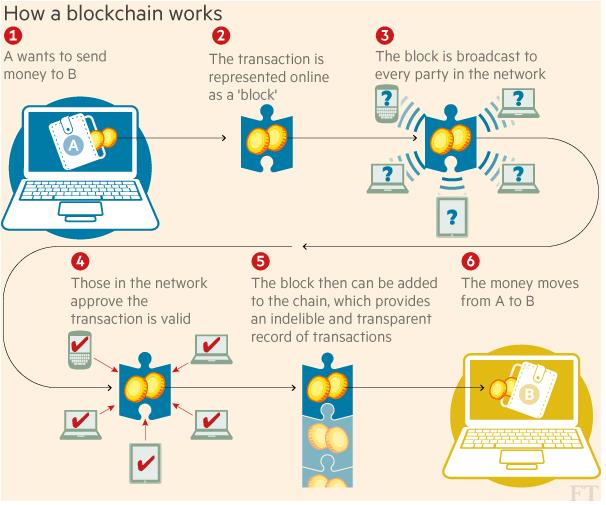

Thousands/millions of computers in a network approve transactions on blockchain. This abrogates the need for human approval in the verification process therefore curtailing human error and producing an accurate record of information. If by probability one computer in the network were to make a computation error, it would be only in that one copy of blockchain.

For the error to spread, the error should occur in at least 51% of the network’s computers – which can be possible only in theory.

Cost Reductions

In today’s world we need to verify each transaction. Be it a notary to sign an official document, a bank to verify a financial transaction or a minister to witness a marriage. But the advantage with Blockchain is that it eradicates third-party authentication and therefore the associated costs.

We have seen in the recent past that most banks have begun to levy fees for transactions above a threshold. In fact most aspects of banking service comes under the purview of some fee, but with Bitcoin as there is no central authority there is no transaction fees.

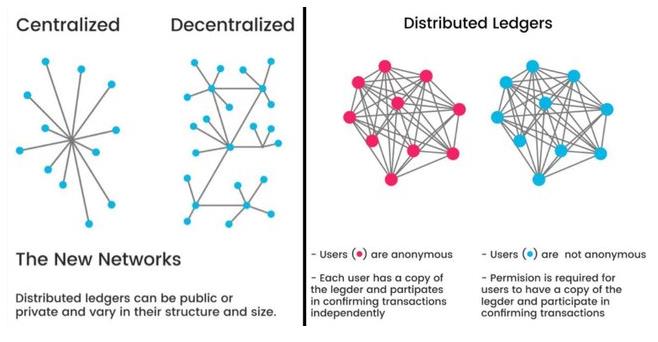

Decentralization

Because Blockchain technology is decentralized it’s pretty much tamper-proof and hacker-proof. Even if a copy of the blockchain were to be hacked, it would only jeopardize one single copy of information and not the network as a whole.

Blockchain does not store information in a centralized location, but info is copied and spread over a web of computers. Whenever there is an addition of a block in the blockchain, every computer updates its chain in the network to reflect the modification. Therefore by spreading information across a network, rather than having one central database the system has guarded itself from interference.

Efficient Transactions

In the financial realm transactions take time to accomplish as there are issues of verification. But the advantage with blockchain is it operates 24/7. Therefore transactions are concluded in minutes and within hours the entire process in deemed secure.

When it comes to international trade, there could be delays due to time, distance and regional disparity. But all this is overcome with the use of blockchain technology.

Private Transactions

Firstly let’s be clear here – blockchain networks are confidential and not anonymous. There are blockchain networks that are public databases and anyone with a Net connection can view the transaction history of a network, but they would not be able to access its details. That is, the identifying information about the users is not accessible.

During a public transaction a unique code called public key is documented on the blockchain and not your personal information. Hence your personal identity is not compromised even though your identity is linked to the blockchain address. Therefore hackers cannot procure your personal information, which is tenable when hacks occur on financial institutions.

Secure Transactions

After a transaction is completed and recorded its authenticity is verified by the blockchain network through the thousands/millions of computers in the network. On validation of a transaction by a computer it is included on the blockchain in the form of a block which contains a unique hash. And the unique hash of the block that succeeds it is also included.

If and when the information on a block is edited, the block’s hash code gets altered, but not on the block that follows it. This characteristic makes it literally impossible for information on a blockchain to be amended without notice.

Also Read: Blockchain In Logistics

Transparency

With very many computers being present on the blockchain network at any given point of time it is implausible to make amends without notice. The blockchain technology is open source and personal information is private. Therefore subscribers can modify a code in the event of having a majority of the network’s computational support backing them. Hence it is evident that tampering with data is farfetched.

Disadvantages of Blockchain Technology

Having expounded the advantages of the blockchain technology, we take you through few negative aspects. The prime glitch to imbibing blockchain technology is political and regulatory. After immeasurable time and revenue being invested in software design and programming, there is hostility to inculcate the technology.

Here are some of the constraints are putting paid to the widespread adoption of blockchain technology.

Technology Cost

Although there is a benefit in fees not being levied for transactions, but Proof-of-Work, or PoW algorithm needs to be completed. This original consensus algorithm in a Blockchain network assists to confirm transactions and create new blocks to the chain. But the downside being it consumes enormous amount of computation power.

In the US the cost to mine a single Bitcoin works out to $4800. But users scamper to validate transactions as when miners add a block to the bitcoin blockchain. Because they get rewarded with bitcoins for their effort. Where cryptocurrency is not enabled miners are compensated through currency.

Speed Inefficiency

Legacy brand Visa of credit cards can process 24,000 TPS (Transactions per second), now – hold you jaw tight or it might drop – the blockchain network can process only 7 TPS. There it is, your jaw dropped. The Bitcoin’s PoW (Proof of work) system takes an estimated 10 minutes to add an new block to the blockchain network. But the other cryptocurrencies such as Etnereum, Bitcoin Cash are a tad better at 20 TPS and 60 TPS respectively. Hence inefficiency is loaded against blockchain technology looking at the abyss of difference.

Illegal Activity

As mentioned in the beginning, every new technology has its downside. Blockchain Technology is susceptible to illegal activity as it protects users from hacks and privacy against all odds. Hence illegal trade activity and unlawful practises are secure too. Users can browse websites without being tracked and make illegal purchase in bitcoins. Silk Road is the apt model quoted for this misadventure, where an online dark web marketplace had been operating for illicit transactions from 2011 to 2013. This was finally shut down by the FBI.

To overcome this debacle, online exchanges in the US now have to collect information from all their customers when they open an account, verify the identity of the customer and confirm that customers are not part of any terrorist group or Red Corner Notice. Now the regulations does not permit full anonymity for users who utilize online exchanges.

Central Bank Concerns

Several prominent banks have launched investigations into digital currency, especially Federal Reserve, Bank of England, and Bank of Canada.

They surmise that research needs to be undertaken to device a process by which the distributed ledger technology could be utilized without hampering financial institutions ability to control currency and ensure safety from explicit or implicit attacks.

Hack Susceptibility

As mentioned earlier, newer age cryptocurrencies and blockchain networks are vulnerable to attacks if they occur above the mean average. But these are profoundly inhibited by the computational power that would be needed to gain majority control of a blockchain network. But studies undertaken by a researcher has indicated that 51% attacks are possible. This is due to the simple fact that hackers now don’t have to own all the equipment needed for the exercise but all they got to do is to rent it.

After an Engineering degree and a Diploma in Management I devoted 16+ years working in the automotive industry. My innate skill and extreme passion in writing, encouraged me to adopt it up as a profession. I have been writing for more than 10+ years in the software industry. The 400+ blogs I published are informative, exhaustive and interesting to a professional and causal reader.